There are two newsworthy aspects of Australia's recent macroeconomic experience:

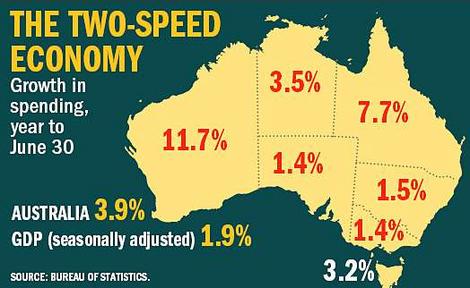

There are two newsworthy aspects of Australia's recent macroeconomic experience:(i) The continuing differential in growth rates between states with a poor performance (the non-resource based 'big' states such as Victoria and NSW) and the performance of the resource-based states (growth rates in Queensland and particularly WA have been stunning). The figure above shows annual growth rates in spending by state and territory. We are becoming a dual economy.

(ii) The disappointing figures on output growth for Australia as a whole. Growth in Australia's output has fallen to its lowest level in 5 years in the June quarter - the ABS reported that output grew by 0.3% per cent in that quarter and 1.9% in the year to June — its worst since the post-GST slump in 2000. From being close to the top Australia has swung close to the bottom of the OECD growth chart.

Higher petrol prices and interest rate hikes seem to have had an impact. In volume terms, Australians have cut spending on petrol and car maintenance by 7.5% since September 2004. Mortgage bills have jumped 14% in the past year and doubled since 2002. Worrying too is the fact that inflation has accelerated to 3.1% in the year to June - this might limit the RBA's ability to keep a hold on interest rates. Some are mumbling the horrible S-word - stagflation.

Other pessimistic interpretations focus on the skill and resource constraints that limit the ability of the economy to expand. After 14 years of sustained high growth and a dramatic reduction in unemployment it is hardly surprising that such pressures are developing in the economy.

But still the poor growth performance is a shock given strong recent growth in employment and new housing approvals.

Non-pessimistic interpretations of recent events suggest:

(i) Recent experience is a statistical blip. This might be true but performance over the past few years has not been flash.

(ii) That business has been running down its stocks in the June quarter and would now need to rebuild them providing a stimulus to the economy - the decline in inventories shaved 0.8% of growth in the June quarter. Furthermore petrol prices have stabilised, at about $1.30 a litre, and the mining investment boom will yield increased exports. The volume not just the value of mineral exports should start to show growth.

The figures showed inflation across the economy accelerating to 3.1 per cent in the year to June. Markets responded by shortening the odds of another interest rate rise in November.

It is early days yet but there is a reasonable presumption that the economy is entering a period of sustained lower growth. This has implications for the next Federal elections although the Howard Government can hardly accept responsibility for bad economic management.

10 comments:

According to Brookesnews the govt is responsible for the inevitable bust that follows the boom of their increased money supply(albeit they are not alone in this). This slowdown and asset price bust is the natural outcome, presaged by increasing overall employment at the same time as manufacturing employment and output was declining. According to Brookesnews this was the typical result of malinvestments caused by too much money supply. The problem is that the real cause will be ignored again, because the Howard govt could never own up to it and so the incoming Labor govt will provide their quack remedy of more IR and 'industry policy' controls. The economy will right itself with rising interest rates(reduced money supply) over time of course and the usual claptrap will take root because of 'at the same time therefore because of' syndrome. Business as usual for elected govts and their love affair with the printing press.

observa, Maybe there is something to this story.

If you look at the RBA chart pack

http://www.rba.gov.au/ChartPack/financial_indicators.pdf

it is obvious we have had very high rates of broad money growth for many years. Since 2002 growth has been between 8-12%. I am no monetary economist but I wonder why no-one worries about this?

Is there no worry because inflation has been seen to be under control? I'd be interested in the views of money policy specialists.

The US picture

http://www.brookesnews.com/062808useconomy.html

and the Australian picture

http://www.brookesnews.com/060708auseconomy.html

If the analysis is right, the bust is just around the corner. The eastern seabord State Labor Premiers may just avoid electorally what the PM can't.

Harry,

The way monetary policy is conducted in Australia (and other industrial countries) is that the interest rate is the instrument variable and money supply adjusts endogenously. Therefore, pointing to excessive money growth means arguing that the cash rate has been too low. I have two issues:

1) Since it is the RBA that adjusts the cash rate I do not see (as Observa suggests) how the GOVERNMENT is responsible for high money growth – especially given that fiscal policy has been well behaved.

2) It is too early to make definite conclusions but there is something about your story. If you look at the credit growth in the business sector it went from 0% to almost 20% between 2002-6. This boom in business credit seems to have been initiated by the reductions in the cash rate in 2000-1 (from 6% to 4.25%) which followed the reductions in the US. Together with the fact that inflation was on target in Australia during that time and stayed on target for another few years (with the cash rate at or below 5.25% till early 2005) the markets seem to have interpreted this as a signal that the neutral rate is lower then it actually is (and previously thought). Hence the credit boom and possible malinvestment. As Friedman would argue it is not the interest rate that tells you about the stance of monetary policy, it is the growth in money supply (and while the link between money and inflation has broken down in low inflation environments the TREND in money growth is still a good variable to look at). Jan

Well jan I doubt Howard would bother trying to pass the buck for an economic downturn onto the Reserve Bank, arguing they were really directly responsible for interest rates and logically the previous low interest rates as well. The Opposition would have a field day with that tack. That's Jackson's complaint. If you as a govt go along the easy money path you deserve everything you get when the inevitable happens.

Jan, I am uninterested in the blame issue but more concerned with what will happen to the economy. You say that monetary policy should be calibrated in terms of interest rates - this seems to me the same thing since you are choosing a price variable rather than a money stock quantity variable - the 'monetary instrument' problem they call it.

So you are saying interest rates have been too low. But in fact they have always been a fair bit higher than those in the rest-of-the-world. And inflation has been low.

I still can't pin down exactly the problem.

Observa,

I guess you are referring to the pre-election campaign and the association of the Liberals with low interest rates as apposed to the ALP with high interest rates. While their point was blown out of proportions it is not inconsistent with the fact that it is the central bank (not the government) that sets interest rates. In my point 1) there is an important qualification regarding the behavior of fiscal policy. If the government is running huge budget deficits it will force an independent central bank to tighten and hence indirectly cause higher interest rates. This is how they should have sold their story. So claiming a part of the merit for low interest rates (as a consequence of disciplined fiscal policy) but then not taking blame when a problem strikes is again not totally inconsistent on paper (but perhaps not very credible in the eyes of the public)...

Harry,

the fact that the rates were higher here than elsewhere is due to relatively higher economic growth in Australia. The rate of growth is reflected in the rate of return and hence in the magnitude of the neutral real interest rate...

Actually Harry Glen Stevens gave a talk on low interest rates once ( it could have been when he was Assistant Governor) and made the point despite being highish in real terms people reacted to the nominal rates as they were too low and hence geared up to the eyeballs.

At present we are merely seeing what happens when there is a once in generation commodity price boom

"At present we are merely seeing what happens when there is a once in generation commodity price boom"

Hmmm, there hasn't been a commodity boom for all countries(eg the US) and yet the monetary growth and asset price inflation has been the same. As Gerard Jackson points out the common thread is growth in money supply, not commodities or fairies at the bottom of the garden. We'll see.

Post a Comment